Just before my 33rd birthday, we informed all our friends, family, and coworkers that we would be taking a year off. It wasn’t our first mini-retirement, but it would be our longest with both of us away from the 9-5. Plus, we were able to welcome a baby, which would put our kid count at five. The general consensus was that people with five kids keep jobs, not quit jobs. So there was a good amount of confusion around our choice.

Often we think about retirement as an age, but turning 65 doesn’t guarantee that you are financially prepared to retire. You might qualify for Medicaid or be able to start collecting social security, but we know that those two things alone do not a comfortable retirement make.

In the Financial Independence (FI) movement, retirement is more of an amount of money than an age. FI is the point in your financial journey where your assets can cover all your expenses indefinitely. A quick way to calculate that is by having 25x your yearly expenses invested. So if you need $40,000 a year to live comfortably, your financial independence number would be one million. Or if you need $80,000 a year, your FI number is two million in assets.

The goal is for all of us to get there eventually. Maybe you reach your FI number at 80, or maybe you reach it at 35. That FI number represents a moment in time. There is a long runway before you get there, and hopefully, a lot of life is left over after you have passed it.

For most Americans, the goal age to hit this FI number is 65. It’s a cultural expectation and what we have seen modeled by family and our communities. In the FI community, that number is often lower. A person might be aiming for 50 or 40, or even 30 years old.

In either scenario, it creates a mental framework that divides life into two segments, before FI (or retirement) and after FI. You’ll hear it in conversations with friends or coworkers, “When I retire, I’m going to get an RV and travel around. Slow travel. Finally, see all those places we never got to visit.” Maybe they have a big list of honey-do projects to handle. Or “We are going to buy a lake house, and I’m spending my weekends on the boat fishing.”

The conversations are remarkably similar in the FI community, although perhaps more adventurous. There is talk about home renovation projects, learning new languages, running marathons, writing a book, traveling through Asia, living in Costa Rica, and time with family and friends.

In both conversations, there is talk about life now and life after FI. All the ways life will be different. All the ways they will be different. Life will be full of friends, travel, personal growth, and hobbies. Most importantly, they will be much, much happier.

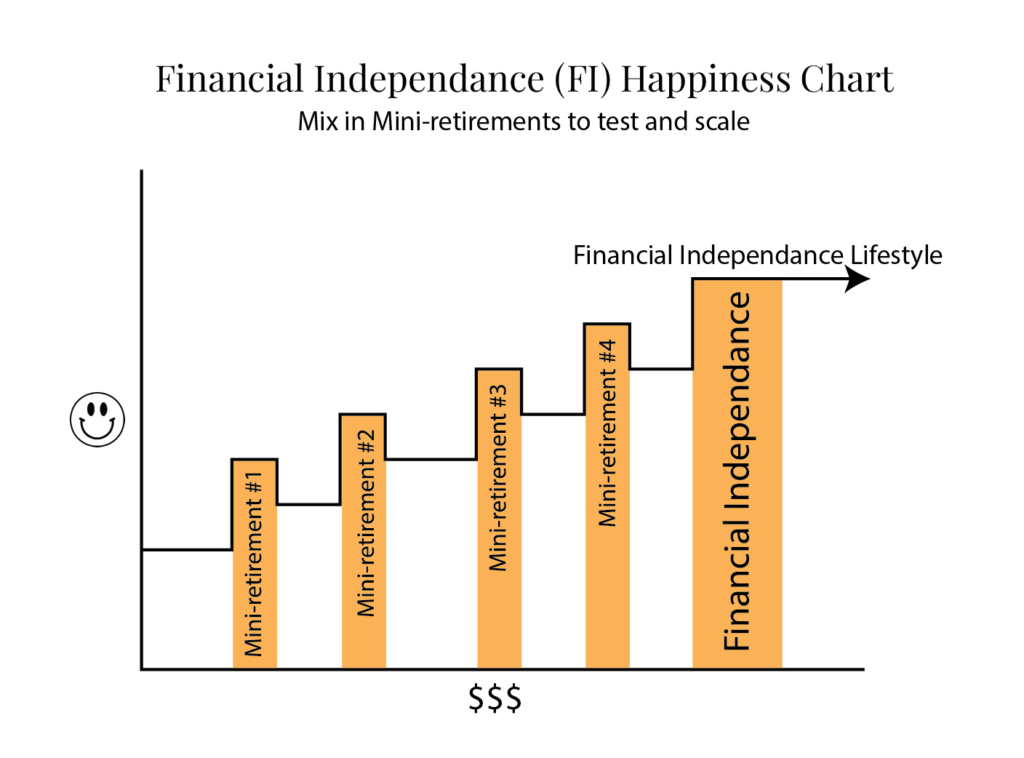

Their chart looks likes this. They are constantly moving forward, growing their financial freedom. Then at one specific point, they become FI, retire and change a whole bunch of things about their life.

Change is Hard

Except…have you ever tried to make a big life change? Turns out change is hard. Uncomfortable. We aren’t instantly successful and competent in that change. There is a learning curve as we develop the skill. While living in Germany, I spent five semesters studying German. Day one was hard. I didn’t get to start the process fluently, enjoying conversations and chatting up the waiter. Turns out day 365 was still hard. I studied two hours a day for two years and struggled the whole time. My German teacher wrote a letter of recommendation for me in which he said that in 30 years of teaching, I had worked harder than any student he ever taught…..and I made the smallest amount of progress for the amount of effort put in. After two years of hard work, I was conversationally fluent with all the seven years old I met. My playground conversation was on point. Not exactly an impressive accomplishment, given the 700+ hours of effort I had invested into learning German.

When you start something new, there is a phase of adjustment. A learning curve. And during that time, what you are doing isn’t going to be effortless, or fluent, or easy. If you have been in your career for a while, you are probably good at what you do. You put in a modest amount of effort, and you get good results.

That won’t be the case when starting something new. The first mile you run won’t be like a seasoned marathon runner’s first mile. The first art class you take will feel clunky and challenging. Your first road trip with a new RV will be full of lessons learned.

By taking mini-retirements, you aren’t attempting twenty changes all at once. With each mini-retirement, you tackle a few changes and build on those in each subsequent mini-retirement. While the change is still a little hard and scary, you take it a bite at a time spread out over the decades.

High Failure Rate

Now think about this chart. You are leaving a career where most of your days are spent putting in a reasonable amount of effort and getting good results. You’re competent and productive. And now you are attempting to change all these things about your life at once. You aren’t just changing one thing; you are trying to change 10 things.

When you try a bunch of new things, you’ll find out you don’t actually enjoy some of them. You won’t bat 100%. So you are also navigating some hard realities about yourself. You don’t actually want to run a marathon. Turns out, even when you have time, you still don’t want to clean out the garage. While some dreams go exactly how you hoped, others have to be let go. You always thought you wanted to write a book, but now you sit down to write, and it’s drudgery. If you never gave yourself the time or space to do a trial run on these goals, you might only have a 50% success rate.

You have postponed so much of life with the hope that “one day” you’ll be able to retire, and then you can make all these changes. Only to discover change is hard, and you don’t really enjoy all the changes you had planned.

The Season Passed You By

Another layer of disappointment can happen when you finally reach FI and retire, and then you realize that the season of life has passed. You were planning to spend a lot more time with your kids, but they aren’t young anymore. Now they are busy with their friends, activities, or even their own jobs and families. Maybe you had hoped to travel all over Europe, but your body isn’t as keen on long flights and walking eight miles a day. And we have all heard the story of people who postponed all their biggest dreams until retirement only to find out they have cancer or pass away, unexpectedly, shortly after retiring.

No matter if you are retiring early or at a more traditional age, postponing your goals and dreams until that one moment has some serious flaws.

Retiring Often

What if we took a different approach? What if you retired often? Periodically throughout your career, you took breaks, a month or longer, to test out some of these goals. You were able to practice this ideal FI lifestyle that you are imagining. You could accomplish the things that are time sensitive, like taking your kids camping while they are younger. Or traveling with your partner to exotic locations before your preferences or health changes.

Spread out throughout your working life; you sprinkle in these mini-retirements. Each time tackle some of the changes you want to make. You practice some new habits; maybe you take up running or learn to meditate. You use the time to focus on your personal growth and improving your communication skills. You take up new hobbies or dive deeper into old hobbies.

The idea of retiring for-evvver can be intimidating. Figuring out how to organize and fill the next 30 some odd years of life is overwhelming. But how to fill and organize a month? Easy. You could probably map that out in the next 30 minutes. How to fill up a year off? That’s doable. If you took a few hours in a coffee shop, you could have a meaningful and productive year off planned.

After each mini-retirement, you will hopefully be able to maintain some of the changes you made. Maybe your new yoga habit sticks around. You learned how to communicate better with your spouse. You have built out your garden and now can enjoy that hobby more on the weekends. You were able to get involved in a non-profit and now serve on the board, which you can maintain while you work your job because it only requires six hours a year. Each mini-retirement increases your happiness a bit. And then the next one builds from there.

While some people love the idea of retirement, others are confused or fearful of the concept “I could never retire! I don’t know what I would do with myself. I would be so bored. I can’t just sit around all day.” And I get it. Most people can’t just sit around all day. That does sound boring. It’s a learning curve to find ways to organize your time, develop hobbies, and find meaning and purpose outside of your work. It takes time, intention, and practice to create a life that you love. You have to figure out what brings you joy. You need to invest in relationships. You need that thing that creates a sense of progress.

I compare retirement to running a marathon. If you have never taken significant time away from a career, it’s like you have never run a race. If your job has been demanding your time and attention, leaving little left over for meaningful hobbies or maintaining a large network of relationships, it’s like you’ve never really even run as a hobby.

So you’ve never run. You’ve never participated in a race. And the first venture in is going to be a marathon. Hum. Any wonder it doesn’t go smoothly? By mile 12 you’re throwing up. At mile 22 you have leg cramps so bad they are carrying you away on a stretcher.

A mini-retirement is like a 5k fun run. It gives you a little taste. A little practice. It’s a small experiment. Plus, it’s much easier to “train” for. A marathon requires a tremendous commitment to training. But a 5k? You can squeeze that preparation in 30 minutes a few times a week. It’s similarly easy to prepare for a mini-retirement, financially and emotionally. You don’t have to save a million dollars to take a mini-retirement. And you can start practicing and preparing for your time off a bit on weeknights or weekends.

Taking a “I’ll just wing it” approach to running a marathon, if you have no experience running, obviously won’t go well. But I see so many people take the same approach to retirement. It’s the mindset of, “I’ll just push hard in my career, stay hyper-focused, and then when that magical time comes to retire, I’ll figure it out. How bad can it go?”

Retiring often can be the antidote. It’s like sprinkling 5k fun runs throughout your life. These mini-retirements are an opportunity to practice. They also let you lean into whatever season of life you’re in. And take advantage of opportunities before they pass you by.

A few years ago, when all my kids were under 12 years old, we took a ten-week trip to 10 National Parks in a pop-up camper. It was an incredible trip, but I also had the feeling that this season of life was about over. They were talking about missing friends more. They were asking if we would have good wifi signal in the National Park. And while the pop-up camper had been a huge upgrade from tent camping, I knew I wanted our next camper to have a bathroom. The middle of the night potty emergencies were inconvenient at best. It was an incredible trip, but I’m really glad we took it when we could. I knew in just five or ten years, life would be different. And while I love traveling with our Jr. High and High school-aged kids, it’s not like traveling with 7-year-olds, who marvel at every public bathroom.

By taking mini-retirements, you can lean into every season of life. These times away from the 9-5 allow you to grow as a person and develop hobbies and interests. You can invest in your relationships. You can enjoy experiences that have expiration dates. Instead of waiting until your FI and hoping to change ten things about your life, you can improve each and every decade of life.

I love all your posts so much. Would you please do a deep dive on what goes into your 25x one years expenses formula vs the often published 10x one years expenses that others have suggested for “retirement”? Im curious about how to think about which formula would make more sense for my situation.

25x your income is based on the 4% rule and the Trinity Study.